Recent

Most read

Most shared

Throughout their careers, as well as being paid via their monthly salary, teachers accrue money that goes towards the pension they receive each year in retirement.

Most workers in the UK get their pensions through what’s known as a “defined contribution” scheme. They and their employer put money into a pot each month that is invested. At retirement, they can choose how much they take from their pot each year, but it’s their responsibility to make sure it lasts for the rest of their life.

The Teachers’ Pension Scheme (TPS), like many other public sector schemes - and a select few private ones - works a little differently. In what is known as a “defined benefit” scheme, teachers still pay in a fixed amount each month but in return they are given a guaranteed fixed annual income for life in retirement.

Because of this, historically the TPS has been seen as a generous scheme, with some even calling the pensions it pays out “gold-plated”.

However, alterations to the scheme in recent years - including a key change back in 2015 - have a major bearing on how much you will get in retirement.

If you joined the TPS from April 2015, you are what is known as a “new” member of the scheme, and your pension is based on the average earnings you make throughout your career.

If you joined before this, your situation is slightly more complicated. More details of how this works - and everything else you could want to know about teacher pensions - can be found below.

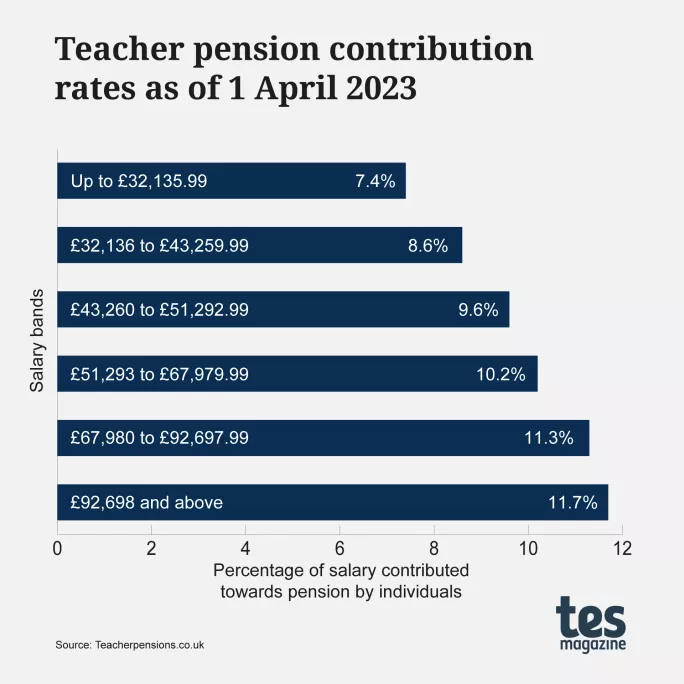

As a full- or part-time teacher, you will pay a fixed percentage of your salary into the TPS every month.

The exact percentage ranges from 7.4 per cent for those earning £32,135 or less to 11.7 per cent for those earning above £92,698.

Full ranges can be found on the TPS website and seen in the table below.

On top of this, your employer contributes 23.68 per cent of your salary into the scheme.

One complaint that teachers often have about the TPS is its inflexibility. Many workplace pension schemes allow their staff to decrease their contributions in return for a lower payout in retirement - meaning that in tough times, like the cost-of-living crisis, employees can receive more upfront cash instead - but the TPS does not allow teachers to do this.

The only option if you want to decrease your payments is to opt out entirely (more on this later).

Other teacher payment information:

TLR payments: how much extra can teachers earn?

PRP: Is the end nigh for performance-related pay?

If you want to pay more, however, you can do this, in return for a bigger annual payout in retirement. There is full information on how you do this on the TPS website.

One thing that is worth noting is that the contributions you make to the TPS are not taxed. They are taken out of your salary before income tax.

If you are working as a full- or part-time teacher in a state-funded school in England and are aged between 16 and 75, then your school must enrol you into the TPS.

Many independent schools also choose to do so - though a growing number are opting not to.

If you’re working at an independent school that is not part of the TPS, it will have to auto-enrol you into a different pension scheme.

Supply teachers employed by an agency will also be opted into a different workplace pension scheme, as long as they are between 22 and State Pension age and earning over £10,000 per year.

Though your school - if it’s in the state sector - must enrol you in the TPS, you can personally choose to opt out.

Unions and many financial experts advise against doing this, simply because the scheme is generous, and opting out means you will miss out on money in your retirement.

If you do still want to do this, you can opt out using a form on the TPS website. Once you opt out, you can then choose to rejoin again, using a separate form.

The amount you are paid in retirement depends predominantly on your salary during your career, and the exact period in which you worked as a teacher.

If you joined the TPS from April 2015 and are in the career average scheme, then you are given 1/57th of your “pensionable earnings” (which includes any overtime pay) each year.

This figure is then added up for each year you have worked and revalued in line with inflation to give you your annual pension amount.

To give an example, if you worked as a teacher for three years and earned an average of £30,000 each year, then in retirement you would get £30,000 divided by 57, which is £526. You then times this by the number of years worked (three) and this means you are entitled to £1,578 each year, which is £131 a month

As another example, if you worked for 30 years and earned an average of £50,000 each year, you would divide this by 57, which leaves £877. Multiply this by 30 and you have £26,310 for the year. Divide this by 12 and it means in retirement you would receive £2,192 a month.

Of course, because this would be revalued in line with inflation, by the time you retire, you will likely get more as a cash sum, but it will be worth the same as £1,578 or £26,310 is today.

If you joined the TPS before April 2015, things are not so simple. There are three different schemes for people who fall into this category.

These are those who were members of the TPS before 1 April 2012, and were a decade or less away from pension age at that date. These people get what is known as a “final salary” pension, and have their average salary at the point they retire (calculated as the higher figure out of their salary in the last year before retirement or the average of the best three consecutive years in the last 10 years) multiplied by their years of service.

If the “normal pension age” (more on this below) when they retired was 60, then their figure is divided by 80. If the pension age was 65, the figure is divided by 60. They then receive this figure each year in retirement, alongside a lump sum equal to three times their annual pension.

These were members of the TPS before 1 April 2012 but were more than 13 and a half years from pension age on this date.

These teachers accrued benefits in the same way as “protected” scheme members until April 2015, and then switched to accruing them in the same way as newer members. They’ll receive a mixture of both types of pension when they retire.

These are the teachers who were members of the TPS before April 2012 but were more than 10 years, and less than 13 and a half years, from their normal pension age.

These people accrue money in the same way as “protected” scheme members but then on a fixed date will start to accrue money in the same way as newer members. If this applies to you, you should have been told this date by the TPS, but if you’re unsure, contact it and ask for your “transition date”.

Different people start getting their pension at different ages - it all depends on when you were born and which type of scheme you are in.

The age at which you start receiving your benefits - which the TPS calls your “normal pension age” or NPA - is generally 60 or older.

For the new members who joined the scheme after April 2015, the NPA is either 65 or your State Pension age, depending on which is the later date.

For those who started before this date, you may, confusingly, have two dates at which you start receiving your full pension.

For the “final salary” element of the pension, if you started teaching before 1 January 2007, then your final salary NPA is 60 as long as you haven’t transferred out, had a break of five years or more, or had a repayment of contributions.

If you started teaching after 1 January 2007, then your final salary NPA is 65.

Regardless of your NPA, you can opt to get your pension a little earlier, though there are disadvantages to this.

Currently, you can start getting your pension at 55 if you’ve left teaching, though you’ll get less money each month as a result. This calculator shows you how the option will affect your pension.

When you retire after working as a teacher, you won’t only get a pension from the TPS.

You’ll also still get your pension from other pension schemes you’ve been a part of - for example, if you’ve worked in other sectors.

You could also be entitled to the State Pension. This is paid by the government and how much you’ll get depends on how many years of contributions you have made to National Insurance - which you pay alongside Income Tax from your pay packet.

If you’ve paid into National Insurance for at least 10 years, you’ll get some State Pension. If you’ve worked and paid in for 35 years, you will get the full amount.

The full amount is currently £203.85 per week, though it increases each year by the highest of inflation, average wage growth or 2.5 per cent, under a policy known as the “Triple Lock”.