Quick View

Quick ViewAQA Accounting - Entire Topic Resource - ACCOUNTING A Level (year 1) - 3.9 Budgeting

This is a PowerPoint presentation lesson resource which covers around 4-5 lessons worth of material on Budgeting.

This is to be taught as part of the first year A Level Accounting Course (AQA) and comprehensively covers 3.9 Budgeting.

The specification content is listed below - and the Presentation is accurately geared towards the descriptors on the specification.

3.9 Budgeting

• The need for budgeting in business organisations: The purpose of budgeting

• The benefits and limitations of budgeting and budgetary control: Benefits of budgeting and budgetary control will include generic benefits as well as the benefits of preparing specific budgets. The limitations of budgeting and budgetary control will include generic limitations as well as limitations relating to specific budgets. Benefits and limitations could include consideration of: zero-based budgeting; incremental budgeting.

• The use of accounting techniques in the preparation and analysis of budgets: The budgets are: cash; sales; purchases; production; labour; financial statements: income statement; financial statements: statements of financial position.

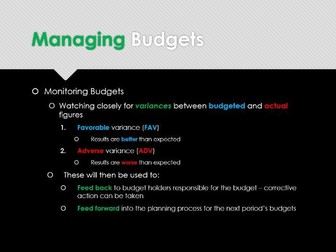

• How budgets are used in planning and control and the calculation and interpretation of variances.

Throughout the presentation are:

• worked examples

• student activities

• explanatory notes

• pros and cons lists (analysis)

• reference to the specification.

This is a ready to use lesson resource that can be edited to the users requirements.